The former Energy Minister, Dr Matthew Opoku Prempeh’s call for the government to exit gas processing is seductive in its simplicity – but it is wrong in its economics, its history, and its vision for Ghana.

There is a certain ideological comfort in the argument that government should simply “get out of the way” and let the private sector do what it does best. It sounds modern. It sounds efficient. It is the kind of prescription that earns applause at academic lectures and donor-sponsored forums.

But when Dr Matthew Opoku Prempeh stood before the University of Ghana’s Department of Political Science and urged the government to stop investing public funds in gas processing infrastructure, he was not offering a radical new idea.

He was, in fact, recycling a doctrine that the world’s most successful energy economies have systematically rejected — one country at a time, one strategic asset at a time. Let us be direct: Dr Prempeh is wrong, and the facts prove it.

ATUABO IS NOT A CAUTIONARY TALE. IT IS A TRIUMPH.

Dr Prempeh criticises the design of the Atuabo Gas Processing Plant, arguing that it does not allow Ghana to fully extract valuable by-products from raw gas. This is a legitimate technical point, but it is precisely the argument for building the Second Gas Processing Plant (GPP II), not for abandoning state involvement altogether. The Atuabo facility was Ghana’s first. You do not discard the architect because the first building could have had better windows.

The Atuabo Gas Processing Plant, commissioned in 2015 and operated by the Ghana National Gas Company, has been one of the most consequential infrastructure investments in Ghana’s post-oil history.

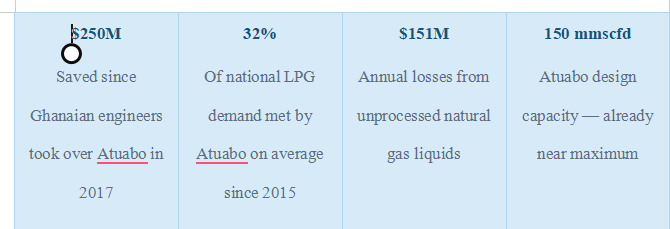

Since 2017, when Ghana Gas transitioned operational control from the Chinese firm Sinopec to an all-Ghanaian technical team of approximately 50 engineers, the country has saved an estimated US$250 million. This is not government propaganda – it is a documented, verifiable fact published by the Ghana Ministry of Information.

Since its commercial operations began, Atuabo has, on average, supplied 32 per cent of Ghana’s national domestic LPG consumption, peaking at 40 per cent in 2017, reducing the LPG import bill by US$47 million in that year alone.

The plant supplies lean gas to thermal plants in Aboadze, Tema, and other industrial centres, reducing Ghana’s dependence on expensive crude oil and heavy fuel oil for power generation. Natural gas is materially cheaper than liquid fuels, delivering lower operational costs to the Volta River Authority and Independent Power Producers — savings that, when passed through, ease pressure on electricity tariffs paid by Ghanaian households and businesses.

To suggest that all of this should have been left to private investors is to retroactively erase a decade of national achievement.

THE PRIVATE SECTOR WILL NOT COME — NOT AT THE SCALE, SPEED, OR TERMS GHANA NEEDS

Dr Prempeh’s position rests on an assumption that, if the government simply steps back, willing private investors will rush in to build gas processing infrastructure. The data on African energy investment tells a starkly different story.

According to the African Energy Chamber, the continent faces an annual energy finance gap of between US$31.5 billion and US$45 billion. External private investment is expected to average roughly US$35 billion per year between 2020 and 2030 — a level that analysts say will not deliver the production growth Africa needs to meet rising domestic demand.

Why? Because private-sector financiers in the post-COVID, high-interest-rate environment face compounding disincentives: ESG pressures pushing capital away from fossil fuels, perceived regulatory and political risks in African jurisdictions, poor infrastructure creating higher risk premiums, and benchmark lending rates in Ghana that hover around 17 per cent — making new gas infrastructure projects extraordinarily expensive to finance commercially.

The Atlantic Council’s analysis is even more sobering: the private sector has historically provided around only 10 per cent of infrastructure funding across the African continent. The remaining 90 per cent has come from governments, multilateral development banks, and public institutions.

This is not a temporary condition that better policy alone will fix. It reflects deep structural realities about risk, return horizons, and the nature of midstream gas infrastructure as a strategic public good.

Ghana is not Norway. Ghana does not have AAA sovereign credit, deep capital markets, or decades of institutional trust that draw private infrastructure investors. As of late 2025, only three of 34 rated African countries held investment-grade credit status. In this environment, waiting for a private-sector-led gas processing solution is not prudent fiscal conservatism — it is strategic abdication.

THE WORLD’S MOST SUCCESSFUL ENERGY NATIONS DID THE OPPOSITE OF WHAT DR. PREMPEH RECOMMENDS

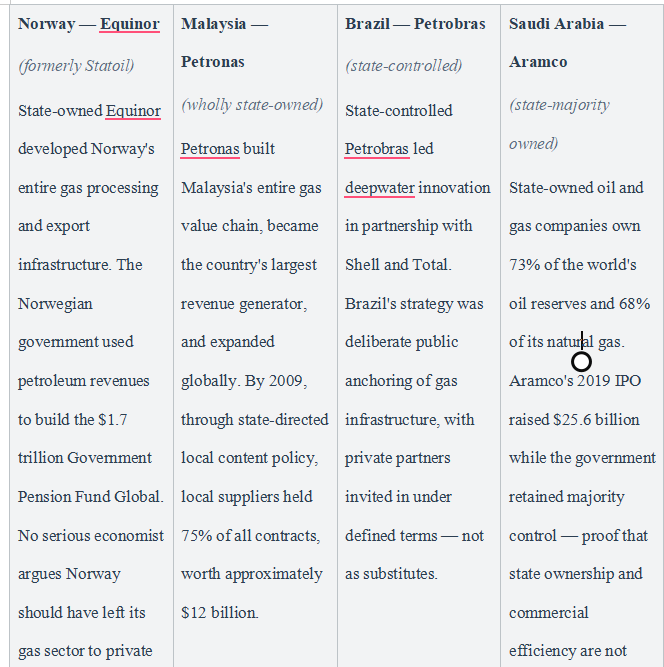

If Dr Prempeh’s logic were sound, the world’s wealthiest oil and gas nations would have privatised their energy infrastructure decades ago. They did not. They built it, and they built it through the state.

Stanford University’s Program on Energy and Sustainable Development analysed National Oil Companies globally and concluded that state-owned enterprises are “often strong drivers of local content” because, unlike purely profit-driven private companies, they can prioritise national mandates involving local workers and suppliers in ways the market would not spontaneously generate.

Ghana’s own Petroleum (Local Content and Local Participation) Regulations, 2013 (L.I. 2204), and its 2021 amendment (L.I. 2435), exist precisely to mandate this outcome. The law requires that Ghanaians be prioritised in employment and contracting in the petroleum industry — an obligation that a purely private, potentially foreign-led gas processing venture would have every commercial incentive to minimise, not maximise.

THE LAW SAYS GOVERNMENT HAS A MANDATE HERE — NOT A CHOICE

Dr Prempeh served as Energy Minister. He knows better than most that Ghana’s legislative framework does not treat strategic energy infrastructure as an optional government hobby. The Petroleum Revenue Management Act, 2011 (Act 815) as amended, establishes a framework for the responsible and sustainable use of petroleum resources for the benefit of both present and future generations of Ghanaians. It is not a framework for delegating strategic resource decisions to investors whose primary obligation is to their shareholders.

The Ghana National Petroleum Corporation Law of 1983, the Petroleum (Exploration and Production) Act, 2016 (Act 919), and the entire scaffolding of Ghana’s petroleum regulatory architecture embed a clear principle: the state is not merely a regulator in the gas sector — it is an active, responsible steward of the national patrimony. GNPC’s mandate as a national oil company explicitly includes participation in the value chain, not simply watching from the sidelines while writing enabling legislation.

THE ATUABO DESIGN CRITIQUE MISSES THE POINT — AND THE SOLUTION IS GPP II

Dr Prempeh’s technical criticism that Atuabo does not fully extract valuable by-products like propane, butane, pentane condensates, and LPG before producing lean gas is a fair engineering observation. But it does not support his conclusion. It supports the opposite one.

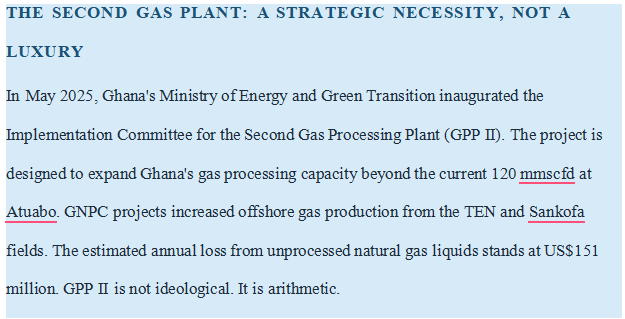

The Second Gas Processing Plant is specifically designed to address this limitation. Ghana Gas has confirmed that GPP II will use turbo-expansion technology to double liquid output, doubling LPG, condensates, and other high-value by-products currently left in the gas stream. When GPP II is completed, it is expected to end LPG importation entirely and save Ghana significant foreign exchange. The project is expected to create approximately 1,500 direct and indirect jobs in the Atuabo enclave alone.

If Dr Prempeh’s concern is that Ghana is not extracting enough value from its gas, the answer is to build GPP II with the right technology, which the government is doing. The answer is not to hand the asset to a private actor who may or may not build it, on whatever timeline serves their return requirements, extracting whatever margin the market will bear.

ON ECG AND PURC: WHERE DR. PREMPEH IS PARTIALLY RIGHT

In fairness, not everything in Dr Prempeh’s speech deserves rebuttal. His call to strengthen PURC and improve ECG’s distribution and revenue collection efficiency is well-founded and broadly shared by sector experts. Ghana’s energy sector debt has ballooned to over US$3 billion as of early 2025, and much of that is attributable to distribution-sector inefficiencies, collection losses, and poorly priced electricity tariffs. These are real problems that demand structural reform.

But the solution to ECG’s distribution problems is not to retreat from upstream and midstream gas infrastructure. These are distinct parts of the value chain. Strengthening PURC, improving ECG’s commercial operations, and building Ghana’s gas processing capacity are not competing priorities; they are complementary elements of an integrated energy sector strategy. One does not fix a leaky pipe by refusing to build the reservoir.

CONCLUSION: STRATEGIC INVESTMENT, NOT STRATEGIC RETREAT

Ghana’s gas sector sits at a crossroads. Offshore fields at Jubilee, TEN, and Sankofa are producing. The Atuabo plant is operating near capacity. A second plant is needed to capture value that is currently being lost — literally burned off or left in the ground. The question is not whether this investment should happen. The question is who leads it and on whose terms.

History, law, economics, and the lived experience of the world’s most successful energy economies all point in the same direction: strategic energy infrastructure in resource-rich developing countries must be anchored by the state, with private capital invited as a partner — not as a substitute for national ownership and control.

Dr Prempeh’s prescription — however well-intentioned — would leave Ghana in the same position as Nigeria, which is Africa’s largest oil producer and yet cannot reliably process its own gas, wasting billions in annual flaring losses.

That is not a model. It is a warning. The state must not retreat. It must build — intelligently, transparently, and for the benefit of every Ghanaian who deserves to warm their home with Ghanaian gas, generate power from Ghanaian fuel, and live in an economy industrialised by the natural wealth beneath Ghanaian waters.

Sources: Ghana Ministry of Energy and Green Transition; Ghana National Gas Company; Ministry of Information, Ghana; Africa Energy Chamber; Atlantic Council; Stanford University Program on Energy and Sustainable Development; Deloitte Africa Energy Report (2025); Petroleum Revenue Management Act 2011 (Act 815); Petroleum (Local Content and Local Participation) Regulations 2013 (L.I. 2204). All figures cited are from publicly available sources.

The writer, Samuel Ackom, is a Broadcast Journalist with Channel One TV and Citi FM

{kind=link}