A surge in CEO confidence is colliding with fast‑evolving risks in Ghana. As technology disruption rises and tariff impacts loom, leaders face a narrow window to convert macro stability into firm-level performance. Here’s what the latest CEO data says—and the decisive moves executives should make next.

Three signals that matter

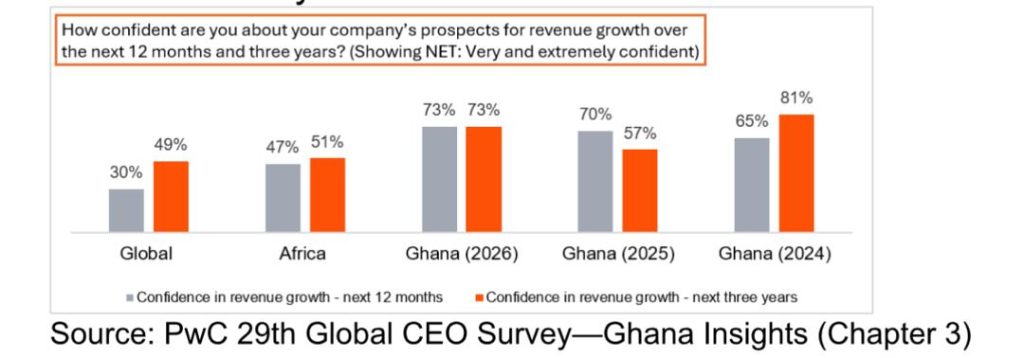

- Confidence at new highs: 73% of Ghana’s CEOs are very or extremely confident in revenue growth over both 12 months and three years.

- Technology risk rising fast: 33% feel highly or extremely exposed to disruption; 48% worry they are not transforming fast enough.

- Tariffs’ indirect bite: only 13% feel highly exposed, yet 46% expect margins to fall due to tariffs in the year ahead.

Seventy‑three percent of Ghana’s chief executives say they are very or extremely confident about revenue growth in the next 12 months—more than double the global benchmark. Yet a third also feel highly exposed to technology disruption, and nearly half expect tariffs to compress margins even though few feel directly exposed. Confidence is surging. Risk perceptions are mutating. And the difference between momentum and missed opportunity will be what CEOs choose to do, next.

The Ghana cut of PwC’s 29th Global CEO Survey offers a clear, if nuanced, message: macro headwinds have eased; optimism is back; the risk map is being redrawn around technology; and the winners will be those who monetise stability quickly while rewiring for an AI‑led, cross‑industry future.

A new optimism—tempered by realism

The mood has shifted markedly. Four in five CEOs in Ghana expect global economic conditions to improve over the next year—up from under half last year and ahead of both global and African peers. At home, falling inflation, a stronger currency and better‑than‑expected GDP growth through much of 2025 and into early 2026 have restored confidence. By March 2026, inflation had decelerated to 3.2%, before ticking up to 3.4% (April), then 3.7% in May. The policy rate had also been lowered from 28% (March 2025) to 14%, signalling a more accommodative environment.

This macro reset is reflected in corporate confidence. Seventy‑three percent of Ghana’s CEOs are very or extremely confident about their company’s revenue prospects over both the next 12 months and the next three years—up sharply from last year’s medium‑term reading. Interestingly, relatively few CEOs appear uneasy about the strength of their leadership benches: only 15% worry they lack the right top team, compared to 21% in Africa and globally.

Ghana CEO revenue confidence hits 73% over 12 months and three years

Share of CEOs who are very or extremely confident in their company’s revenue growth over the next 12 months and the next three years.

Cautious optimism is the right read. Executives in Ghana are acutely aware that currency stability remains fragile and that external shocks—commodity swings, geopolitical tension, supply chain disruptions—could quickly test the recovery. They also see an inflection point in business fundamentals: the blurring of industry lines is now a durable feature of the landscape, and the “Great Reconfiguration” of value pools is real. That reality is already in the numbers.

Cautious optimism is the right read. Executives in Ghana are acutely aware that currency stability remains fragile and that external shocks—commodity swings, geopolitical tension, supply chain disruptions—could quickly test the recovery. They also see an inflection point in business fundamentals: the blurring of industry lines is now a durable feature of the landscape, and the “Great Reconfiguration” of value pools is real. That reality is already in the numbers.

“Equally important, this cautious optimism also underscores CEOs’ admission—perhaps, not overtly—that they need to do more at company levels to ensure they position their companies to convert the opportunities that a good macro-economic environment might spawn.” — George Arhin, Partner, PwC Ghana

The risk map is shifting—towards technology

For the third year running, macroeconomic volatility ranks among CEOs’ top short‑term threats. But this year, technology disruption has risen rapidly on the risk register, overtaking inflation and cyber as a near‑term concern. Thirty‑three percent of Ghana’s CEOs say they feel highly or extremely exposed to tech disruption in the next 12 months. Many worry they are not transforming fast enough to keep pace, with 48% anxious about safeguarding their company’s medium‑to‑long‑term viability.

That anxiety is well placed. AI’s potential is accelerating—and unevenly distributed. Eighteen percent of CEOs in Ghana say they are already getting full value from AI, while nearly four in ten report they are experimenting but have yet to see material financial impact. The implication is clear: first movers are banking real P&L gains while many are still in the lab. The longer the gap persists, the harder it will be to catch up.

There is another, subtler tension: an apparent underweighting of cyber risk even as technology disruption climbs. It is tempting to treat cyber as an IT issue rather than a board‑level threat. That would be a strategic error. As businesses scale digital and AI, risk exposure compounds precisely where governance is weakest.

Tariffs: low exposure, high impact?

Tariffs present a revealing contradiction. Only 13% of Ghana’s CEOs feel highly exposed to tariff‑related risks—less than in Africa or globally. Yet 46% expect tariffs to reduce net profit margins in the next 12 months, compared with 31% in Africa and 29% globally. The message isn’t that tariffs don’t matter; it’s that their impact is indirect and cumulative—via higher input costs, squeezed competitiveness and weaker trade flows. Leaders may not feel the sting daily, but they expect a dent in earnings.

This pattern—optimism, anxiety and ambiguity—runs through the data. CEOs are upbeat on growth. They recognise technological disruption is accelerating. They see margin pressure from global policy shifts. And they are still calibrating their exposure and response.

Cross‑industry innovation moves from talk to traction

If there is a bright spot in execution, it is the pace at which Ghana’s CEOs are stepping beyond traditional sector boundaries. Thirty‑six percent report that more than one‑fifth of last year’s sales came from product or service innovations developed outside their historic industry lines over the past three years. Another 39% say more than one‑fifth of 2024 sales came from offerings introduced over the last five years. Appetite for reinvention is building: 68% plan to grow beyond their current industry boundaries over the next three years, with 23% eyeing transportation and logistics—a sector embedded in the “How we move” domain and a node where value is rapidly reconfiguring.

This diversification reflects the “domain” logic reshaping markets: growth opportunities are increasingly organised around human needs—how we move, feed, build, care, connect—rather than the old industry silos. For CEOs, the strategic question is less “Which sector?” and more “Which domain roles can we credibly play, and how do we orchestrate or participate in the ecosystems that serve them?”

Why time suddenly matters more than ever

One data point deserves the full attention of boards: how CEOs allocate their time. In Ghana, leaders report spending 52% of their time on short‑term issues—operational tasks, urgent decisions, day‑to‑day execution—compared with 47% globally. That skew may be rational amid shocks. But it undermines future‑readiness if it crowds out medium‑ and long‑term agenda‑setting: sharpening the company’s “where to play” and “how to win,” building technology capability, re‑platforming operations for speed, and institutionalising foresight and scenario planning.

Executive time allocation is strategy. If leaders don’t deliberately rebalance calendars toward future‑building, the organisation won’t either.

AI is delivering—if you treat trust as a design principle

The survey suggests a two‑speed AI reality. A vanguard is extracting value; many are still experimenting. The difference often lies in governance and capability. Companies that elevate AI as a board‑level topic, adopt Responsible AI frameworks, uplift data governance, and deploy 1–2 high‑impact use cases with clear KPIs start to build confidence and momentum. As maturity grows, they expand to 3–5 scaled use cases, invest in Machine Learning Operations (MLOps)—or partner credibly, upskill the workforce and plan for data localisation. Over time, they embed AI into products, services and decision systems—and build proprietary data assets that compound advantage.

This is not a technology choice alone; it is a trust and competitiveness agenda. In an AI‑led world, responsible design, governance and data strategy will be control points.

The cost of complacency

The macro window is open. But it won’t stay that way. Currency stability can reverse. Tariff regimes can shift. Technology curves will not wait. The risk of ignoring the signals is straightforward: missing the window to turn macro stability into firm‑level performance; widening the gap versus AI‑enabled competitors; and anchoring the business in static cost structures and brittle supply chains as shocks recur.

Conversely, the opportunity is immediate and compounding. Disinflation and rate cuts create space to tighten pricing discipline, unlock productivity, and rebalance product and services mix. Supply reconfiguration—local sourcing where viable, supplier diversification, regional revenue hedges—can reduce volatility exposure. And a faster path to innovation, underpinned by strong portfolio governance and kill criteria, can accelerate time‑to‑market and speed the shift to growth domains.

A note on climate: prepare the model, not just the message

Some CEOs in Ghana are confident they have processes to account for climate opportunities and risks. Yet the country remains acutely climate‑vulnerable, and global markets are increasingly sustainability‑sensitive. The strategic imperative is to embed sustainability‑by‑design into business and operating models—not to treat it as a separate reporting exercise. Over the medium term, sustainability and competitiveness will converge.

The opportunity in M&A: a launchpad for capability

Ambitions are rising, but capital allocation remains cautious. That needn’t be a constraint. In a capability‑scarce environment, M&A can be a disciplined way to acquire critical technology, IP, talent and data that would be slow or costly to build. The litmus test is strategic fit to the chosen domain play, not deal volume. Where balance sheets are tight, partnerships and corporate venturing can achieve similar capability lift at lower capital intensity.

Strategic implications: what should be Ghana’s CEOs’ next moves

The survey’s core message is not merely diagnostic; it is prescriptive. Here are the priorities Ghana’s CEOs should act on—now.

- Monetise macro stability at the firm level. Macroeconomic tailwinds don’t automatically translate into earnings. Convert them deliberately through tighter sales and operations planning, dynamic pricing, and a sharper product/service mix. Strengthen cash discipline while investing in demand‑sensing capabilities—including AI‑enabled analytics—to match supply to shifting market signals in real time.

- Hardwire financial resilience into your operating model. Treat treasury as a strategic hedge function. Formalise FX risk frameworks; deploy currency clauses; build natural hedges via regional revenues; and explore selective vertical integration where it improves cost control or access to critical inputs. The goal is to absorb volatility within your operating model—not react to it after the fact.

- Choose your domains—and your ecosystem role. Reinvention starts with strategic choice. Define the domain(s) where you can win and the role you will play—platform orchestrator, capability specialist, or niche integrator. Articulate a platform strategy; acquire or build critical technology; secure anchor customers; and tap blended financing to accelerate scale. Guardrails matter: set clear return on invested capital thresholds for bets, and install portfolio governance with explicit kill criteria so capital recycles quickly from what isn’t working to what is.

- Make AI a board‑level, trust‑led capability. Move from experimentation to impact. Elevate AI to the boardroom; adopt Responsible AI; uplift data governance; and prioritise 1–2 use cases with measurable KPIs to prove value. Scale to 3–5 as capability builds; invest in MLOps or partner to acquire it; and upskill the workforce at pace. Plan for data localisation and start building proprietary data assets—these will be tomorrow’s moats.

- Rewire for speed and resilience. Redesign your operating model to compress time‑to‑market. Diversify suppliers and improve end‑to‑end visibility. Where viable, build regional manufacturing or local content capability to reduce import dependence and logistics risk. It’s not resilience versus efficiency; it’s resilience that unlocks efficiency.

- Reset leadership time and incentives. Rebalance CEO and executive calendars so at least half of leadership time focuses on medium‑to‑long‑term priorities. Institutionalise quarterly “future” decision forums with key stakeholders, align incentives to innovation and reinvention milestones, and define forward‑looking KPIs—AI ROI, launch velocity, percentage of revenue from new offerings. Establish a future‑oriented Project Management Office (PMO) to coordinate execution across the enterprise and embed scenario planning into decision routines.

Conclusion: optimism with a plan

The data is unambiguous. Confidence is back. Risks are evolving. And the window to turn macro stability into competitive advantage is open—but not for long. Ghana’s CEOs can seize it by doing three things at once: monetising tailwinds through pricing and productivity; rewiring their business and operating models for an AI‑led, cross‑industry future; and refocusing leadership time on building what’s next.

In a world where technology resets competitive baselines and shocks recur, advantage goes to the prepared. Confidence without conversion is a story of what might have been. Confidence with a plan is a strategy for the decade.

Note:

This article was authored by Vish Ashiagbor (Country Senior Partner, PwC Ghana) and Richard Ansong (Partner, PwC Ghana) with contributions from Kwame Ansa Akufo (Lead, Thought Leadership, PwC Ghana) and Edwin Ntiamoah (Senior Associate, Thought Leadership, PwC Ghana).

For more details, you could access the full report (29th Global CEO Survey – Ghana Insights) at www.pwc.com/gh.

{kind=link}